Should I invest in ETFs myself or through a Private Pension Plan in Germany? Free Investment Calculator.

Do you know the annual tax rate on ETFs held through a broker account, the cost of rebalancing your portfolio, and the average loss from self-investing? Find out if investing in ETFs through a broker makes sense for you, or whether the alternative of a low cost Private Pension Plan with a professional ETF portfolio is better.Updated on 3 September 2025

Let’s calculate whether you should invest into ETFs directly or through a Private Pension Plan (PPP)

The results of our comparison IF you invest as well as we do:

Total assets at 67 if you invest in ETFs directly: 430.129 € | Total assets at 67 if you invest through a PPP: 443.912 € | Relative savings per year by investing in a PPP: 0,13 % |

The results of our comparison IF you are the usual investor:

Total assets at 67 if you invest in ETFs directly: 274.363 € | Total assets at 67 if you invest through a PPP: 443.912 € | Relative savings per year by investing in a PPP: 6,21 % |

Let’s give you further recommendations as to what to do:

Our recommendation:

You are a small investor: keep investing through a broker till you hit at least 10.000 € and are ready to save at least 100 € per month. This is because, as a small investor you benefit from the tax-free threshold of 1200 €. Moreover, if you can only contribute a modest amount each month to a private pension that will lead to higher fees for the pension plan. When you are ready to invest more, a private pension plan can really help especially because of substantially higher investment returns.

Let us discuss the numerical results in more detail. If you manage to have exactly the same portfolio as Pensionfriend, you will have 430.129 € at 67 compared to 443.912 € when you invest through a Private Pension Plan. Investing through a Private Pension plan will save you 0,13 % per year on average, or a total of 13.783 € until 67. This is because your capital gains taxes reduce your return by about 1,12 % per year when you invest directly.

If you invest like the typical investor, you will have just about 274.363 € at the age of 67, compared to 443.912 € when you invest through a low-cost high performing Private Pension Plan. Indeed, this is a huge difference. All studies point out that individual investors perform much worse than professionals.

Biases in individual investors are well documented, such as self-attribution bias assigning success to oneself, familiarity bias with a focus on investment that one knows, and being overwhelmed by choice, which leads to inaction. As an individual investor, you don't have the time to find, for example, to find the tracking difference of ETFs or compare the indices in an unbiased way. The key is to find trustworthy yet low-cost professionals that do it for you. And that is what we aim to be.

For well-performing investors, keep a few things in mind: the more you adjust your portfolio, the better a private pension plan is: you pay no taxes on buying or selling any ETFs when you have a PPP. When you make your decision, also consider how the future may change your decision:

The costs of our Private Pension Plan are decreasing with the size of your assets, as we promised.

If you change your portfolio later in life — as it is typically advisable — this would be very costly in terms of capital gains taxes if you hold it with a broker.

The so-called free brokers like Scalable Capital and Trade Republic have significant external funding of 1-4 % of their assets. These investors want to see returns of 3X to 10X on their investment, which will, in due course, lead to higher fees.

In the following graph, we compare investing directly in ETFs to investing in the same ETFs through a tax shield and holding the retirement plan until retirement. The numbers are after taxes. We added investing in the MSCI World through a broker as a benchmark to highlight that it is most important to invest well. At Pensionfriend, we aim for 8 %, which is 2 % over the MSCI World index.

Remember that most individuals perform much worse than the benchmarks and are better off delegating the management of their portfolios. Trade Republic, which has over 4 million users, shared data on the performance of 216.000 early users in what they call the largest-ever study of retail investors. Those data show that their average investor had returns of 7,1 %, but it was when the S&P 500 had a record return.

In particular, in the last year of the study, when 80 % of the respondents joined, the S&P 500 returned an astonishing 52,47 % (April 1, 2020–April 1, 2021). These respondents, grouped by starting period, had annualized returns of 0 % to 10,7 %. That is less than a fifth of the market return. This underlines the finding in the literature that individual investors strongly underperform the market. We estimate at least 3 %. But frankly speaking, the 5 % used as a return for self-investing is, in most cases, too optimistic. It also underscores that individuals take far more risk and hence experience much more volatility in their returns as well!

This is by far the most important reason to delegate the management of your portfolio to professionals, especially if these professionals charge you tax benefits offset little and their fees.

The six main tax benefits of a Private Pension Plan

You do not pay the annual ETF withholding tax (Vorabpauschale) of currently 0,33 %.

You pay capital gains tax only once with a private pension plan, namely when you take out the money. We call this the tax shield effect. If you would instead have an ETF portfolio with a broker, you pay tax every year on the gains you realize if they are higher than the withholding tax.

15 % of your capital gains are tax-exempt in line with § 20 4 of InvStG whenever you take them. For an ETF held through a broker in stocks, this is 30 %, while an ETF in bonds has a similar 15% exemption.

Only half of the remaining gains on your investments are subject to taxation if you have it paid out as lump sums from the age of 62 onwards and if you have held the pension contract for more than 12 years. This is referred to as Halbeinkünfteverfahren and is regulated in § 20 6 of EStG (the German income tax law).

Your partner or whoever you assign as the beneficiary of your PPP in case of your death pays no capital gains tax of 26,375 % because it is treated as an insurance payment. We estimate the annual value at about 0,25 %.

If you decide later in life to take your PPP, you will want to stop taking out lump sums but convert the remaining amount into a fixed monthly pension, called an annuity. Your effective tax rate falls to a few percent.

Benefits 2. 3. and 4. together means paying tax once at a rate of 42,5 % = (1–15 %) × (1–50 %) on the gains if you are over 62 and held the contract for over 12 years.

For those who want to know it more exactly, the tax rate is the minimum of (1–15 %) × 26,375 % and (1–15 %) × (1–50 %) × income tax rate in retirement. For a median gross income,that income tax rate is about 19 %.

It follows that the tax rate is (1-15 %) × (1-50 %) × 19 %, which is just 8 %! For an income of 60.000 € gross, the tax rate on your gains is about 12 %. This compares to a normal capital gains tax of 26,375 %.

If you take the payment as an annuity or a fixed monthly pension, the income tax rate is reduced depending on your age. It is reduced by 83 % if you take it at the age of 67 and, for example, by 90 % if you take it at the age of 77. So at age 67, your tax rate of 30 % becomes 5,1 %, and at age 77, it becomes 3 %. Remember that you pay it over the entire amount, including the invested sum. But for most people, that difference is modest.

What are the tax and cost considerations to take into account when you hold ETFs through a broker:

If you hold an ETF that is over 51 % invested in stocks, you only pay 70 % of the tax according to § 20 1 of InvStG. If it is a mixed fund with under 51 % in stocks, the tax rate is 85 %. The impact of these two rules together is that for a stock ETF, you pay a withholding tax of 0,33 % and an overall capital gains tax rate of 18,4625 %.

According to § 18 of InvStG, ETFs are subject to a withholdings tax. This tax depends on the interest rate, which was basically zero for a few years as interest rates were so low. For 2023, the rate used for the withholding tax has been set at 2,55 %. This was the interest rate at which the 15-year German government bond traded on the last trading day of 2022, December 30. This rate is multiplied by 0,7, and any ETF holder must pay this tax over last year's holdings.

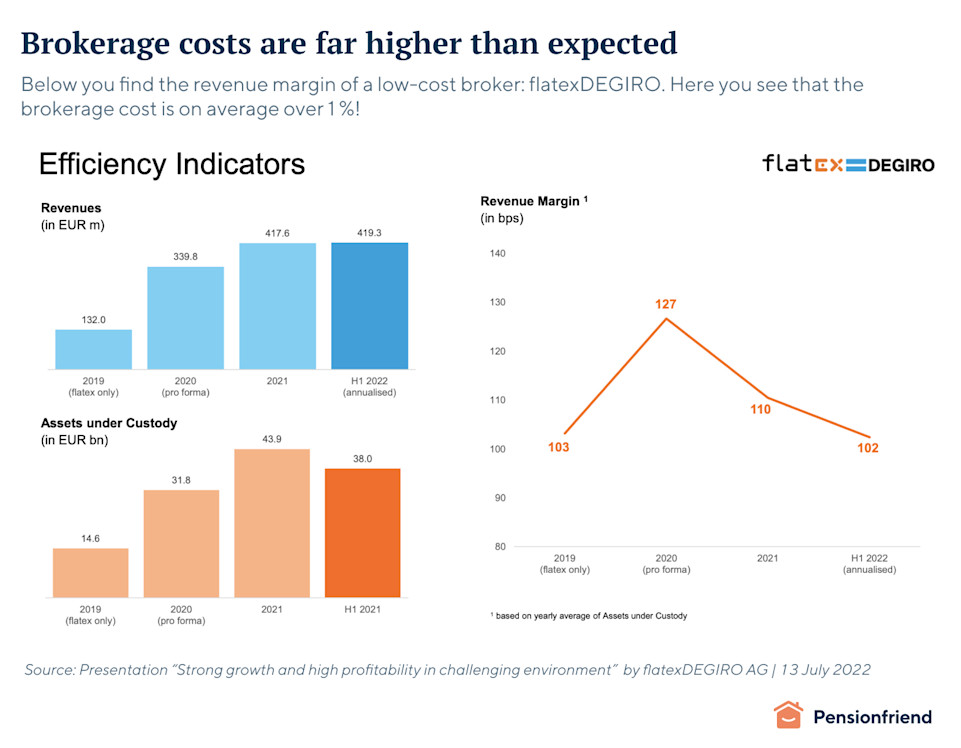

For a stock ETF (with the additional 30 % deduction), this means a charge of 26,375 % × 0,7 × 0,7 × 2,55 % = 0,33 %. This tax is, in the end, deducted from the capital gains tax you report when selling your ETF, but it means that, in the meantime, you have less capital working for you.You will be surprised to find out how much money brokers effectively cost. They have a great way of hiding it, for example, in trading margins. Keep in mind that they need to make money somehow. In their annual reports to shareholders, they are, however, very proudly displaying how much they earn from their customers. Below, you see a figure from an investor presentation in 2022 of one of the lowest-cost brokers, which shows that they earn over 1 % on their client’s assets on average.

Our underlying assumptions

How do we deal with these complexities in our calculator? First, we assume that the withholding interest rate stays at 2,55 %, although there is a risk it could increase. Second, we assume that the broker charges 0,2 %, which is a fifth of the overall revenue they obtain from clients, but we assume that you are getting a great deal.

We contrast this with Pensionfriend's fees for a Private Pension Plan of 0,69 % annually of the value of the assets. For portfolios over 250.000 €, the overall fee declines to 0,49 %. There is no upfront or withdrawal cost.

We assume zero buy-and-sell cost of ETFs — they are zero for Pensionfriend. We assume a gross retirement income of about 60.000 euros (and in line with that, a tax rate of 26,375 %, equal to the capital gains tax rate).

For a monthly contribution of 300 € at age 30, increasing annually at 5% with payout at age 67, and a return of 8 % – in line with the expected return for our flagship portfolio – this results in effective costs for a private pension plan of 0,61 % before the end tax and 1,03 % after the end capital gains tax. This excludes the benefit of no capital gains tax for any beneficiary in the case of your untimely death.

Holding ETFs through a broker in this same portfolio and adjusting 10% of the portfolio each year results in an effective cost of 0,86 % before the end tax and 1,24 % after the end tax.

You must choose low-cost private pension insurance to take advantage of the tax shield. Most products in the market have high costs. Costs per year are as high as 4 %! The above example uses our own low-cost product with a fee of well under 1 %.

Lastly, an added benefit is that your ETF-based private pension plan is seizure-proof, so you can't be forced to sell it if you should ever receive state welfare benefits.

Secure your retirement with Pensionfriend's flexible and tax-efficient pension plan.

The clever way to invest and retire in Germany

Secure your retirement with Pensionfriend's flexible and tax-efficient pension plan

Selecting the right ETF to track an index matters!

You might expect that every ETF that tracks an index, for example, the S&P 500, has the same performance. That is not the case! You can find ETFs that outperform slightly but robustly and those that underperform significantly. Selecting the right ETF for your index is pretty important.

We review in detail which ETFs in a given class perform better, including all costs and hidden gains. For example, for the S&P 500, we save an expected 0,25 % compared to the index by picking ETFs that outperform the index in a quite reliable way, that is, 3 out of 4 quarters.

ETFs that outperform irregularly indicate active management, which is a red flag as it is unlikely to lead to outperformance in the long run – as finance research shows – and instead often means higher cost.

Choosing the right index or benchmark is crucial

As professionals will tell you, 95 % of your return is about picking the appropriate benchmark or basket of indices you want to track. A disciplined investor has such a benchmark and then tracks under or outperformance.

But short of going all the way, let's first just be realistic and avoid the many big pitfalls:

As a long-term investor, do not fall into the trap of the many guaranteed products. Eventually, a good index is safe. We see so many examples of guarantees that ruin the returns.

Do not choose an index based on short-term data. We look at total return data over the lifetime of the index and compare them to indices for which we have the longest time series (of up to 150 years). That gives you hard insights as to under/outperformance.

For example, the MSCI World Index has shown an 11 % return since its start, and everyone nowadays seems to think that that is the best choice. High return, well spread. But this period was just a very good period for stocks and included relatively high inflation. Other indices, like the S&P 500, outperformed the MSCI by 1 %. More fundamentally, 11 % is not a sustainable stock return. A sustainable stock return is about 7 %: the sum of nominal gross domestic product growth plus dividend yield/stock buybacks. If the return were higher, companies' profits would take up the entire GDP, which would not work.

We have some tools to help select a benchmark based on long-term returns and risk to the indices (based on historical data and fundamentals).

Why rebalancing?

In case you are wondering if you should trade your portfolio at all, virtually anyone will want to adjust their portfolio over time based on their benchmark. This is what the profs call rebalancing. So, if you have two ETFs with an ideal weight of 50 % each, then, for example, at year-end, you find that due to price movements, the weights have shifted to 40-60. At that point, pros would rebalance the portfolio back to 50-50, which involves selling some of one ETF and buying some of the other.

The profs do this, as most good indices over time display some mean reversion. So, selling the expensive and buying the cheap index, then, over time, an extra gain as you usually sell high and buy low.

We checked the finance literature and tested which algorithms for rebalancing work best. We created one that leads to a small outperformance, in addition to creating a more steady portfolio and taking away the headache of adjusting the portfolio yourself.

Rebalancing also makes sense when you get older or want to de-risk for other reasons. Shift towards more stable investments, like ETFs that hold rented properties.

Also, if interest rates increase, bonds become more attractive, requiring a shift in your portfolio. This involves buying and selling ETFs, and a tax shield like PPP helps you preserve your capital.

The biggest risk for individual investors

Individual investors' biggest risk is succumbing to fear or greed. Buy when stocks have gone up, which is also known as FOMO, the fear of missing out. And the fear that losses will continue when prices are down. In contrast, studies are not conclusive as to the size of the losses – as they depend on the market circumstances — credible studies indicate that investors lag 3–4 % compared to the country benchmark.

We also see repeatedly that individual investors do not choose the best index. Unfortunately, we also see many unscrupulous advisors put their clients in portfolios with large hidden costs.

Few individual investors – and even many professionals – do not understand which currency they should pick for their ETFs and what difference it makes. This can amount to 2 % annually. We urge you to seek a portfolio review.