Net Return: The Real Way to Calculate Returns

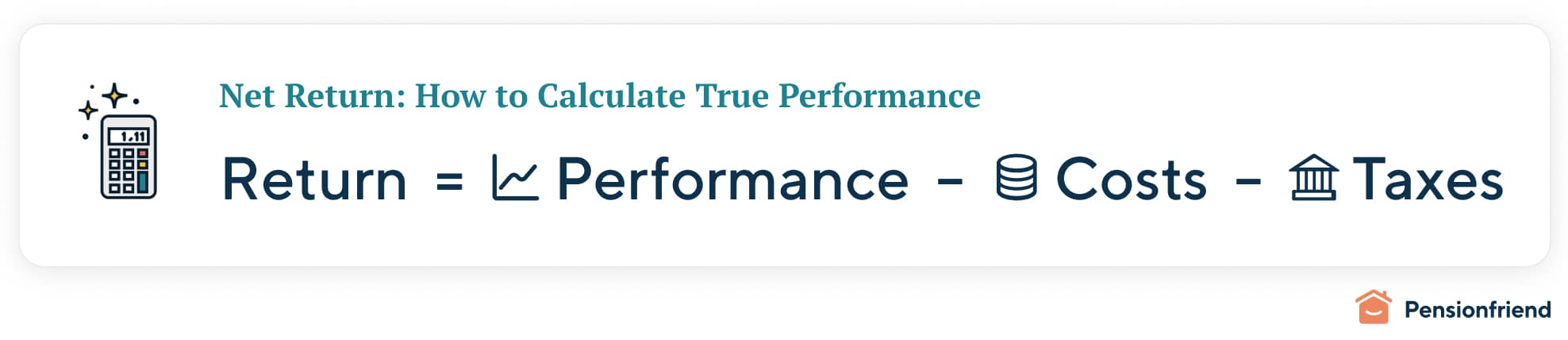

Performance is the most important aspect of generating a good pension. When evaluating the performance of our pension plan, we focus on net return, which considers performance, costs, and taxes. Compared to other retirement plans, such as company pension plans, which are constrained by investment requirements that yield low returns, Pensionfriend's Pension Plan aims to achieve a higher net return and, thereby, a better pension.

For example, the expected net return of Pensionfriend's Global Outperformance Portfolio is about 6,7%, calculated as 8,30 % performance minus 0,49 % — 0,69 % costs, minus 0,25% ETF costs minus 0,48 % tax. The exact tax costs depend on your age. In comparison, the net return for a typical company pension plan is only 0,5 %, derived from 2,5 % performance minus 2 % expenses and 0 % net tax benefits.

This example shows how important return is.

At Pensionfriend, we prioritize outperformance and long-term safety when constructing our portfolios. We believe in the value of investing in broad-based stock indices and the ETFs that capture them at low cost. Stock picking and active management do not create long-term safety or return, as history and plenty of finance studies show: Trying to jump all the time between boats to catch the fastest moving ship leaves many people swimming and only a few lucky. At a fundamental level, stocks will grow with the economy, and this is what ensures that they are safe.

The key challenge we tackle is identifying the broad-based indices that best capture global growth reliably. To do so, we rely on past performance as the best indicator of the future. However, we rely solely on past performance that is properly measured, compared, and unbiased, with evidence that the factors underpinning outperformance are persistent and in line with economic and finance theory and literature.

This is what decades of investing, working with the largest investment funds, and training thousands of professionals in charge of trillions of public investments have taught us.

Curated Portfolios Based on Best Practices and Longest Unbiased Data Analysis

In line with this, we focus our selection of stock indices on countries and regions, as this is the most persistent source of performance. By analyzing the deepest and most prolonged return divergences across regions, we can pinpoint the likely indices to excel. Regional factors such as population growth, government institutions, market size, and openness are vital in determining long-lasting economic performance. These regional dynamics are not easily arbitraged away, leading to persistent out or underperformance.

When choosing our preferred indices, we prioritize absolute performance over day-to-day performance or annual volatility. For risk, we focus on maximum drawdown, that is, the maximum decline of the portfolio and securing the best minimum and expected pension. For a long investment horizon, the best performance goes hand in hand with the highest minimum return: the better performers recover quicker and better. This aligns with the investment horizons of our clients, particularly those with longer-term goals.

To ensure unbiased data analysis, Pensionfriend relies on the longest available data series, spanning over 150 years. This approach eliminates data bias caused by selectively picking specific periods of performance. In cases where shorter data sets are available (which is common, as many indices have only 20–50 years of history), we compare them against the longest data sets.

Our approach avoids data mining and survival bias. We avoid investment strategies, such as market timing, sector rotation, dividend stocks, and growth strategies, as they tend to be unreliable and do not produce consistent high performance; instead, they create additional cost and risk. In addition to regions, we focus on small capital indices as these are the only strategies we identify that tend to have persistent outperformance due to the innovative character of small companies. They come with higher volatility, but that is offset by quicker recovery.

The best portfolios are our global portfolios. In addition to the expected return of about 8 %, we expect over the long run a small appreciation of the currency to add to the value. For those investors with a so-called home bias – they like to invest in their currency and own region – we have identified a superior Euro portfolio that outperforms the standard German (Dax) and European (STOXX 50) indices by a wide margin and, similarly the MSCI World index in Euro.

To operationalize the investments in the stock indices we have selected, we choose Exchange-Traded Funds (ETFs) with a high probability of outperforming the index. We review for consistent small outperformance, net of cost. The underlying logic is that smart ETF managers keep the costs of tracking the index low while making a little extra, for example, by not buying all 500 stocks in an index but just 480 and by anticipating changes in the index. Some managers take far too much freedom, adding costs and reducing performance.

We also don't look for sizable outperformance here, as it indicates that managers take considerable risks. At the same time, such active management cannot be expected to lead to persistent outperformance – the standard result in finance literature. However, seeking out small regular gains while keeping costs relatively low is possible. Altogether, this is reflected in the so-called tracking difference, which we study closely. We pride ourselves on being fairly unique compared to others offering supplementary pensions in Germany.

We aim for ETFs that outperform the index before cost by about 0,25 % and then for the lowest cost for the relevant index.

More Small Wins and Ease of Mind: Rebalancing

In addition to our index and ETF selection strategy, we use a smart rebalancing algorithm to enhance the performance of our portfolios. This adds some extra performance to Pensionfriend's Pension Plan, which offsets costs and generates higher returns for you.

As prices change, the weights of the different ETFs in your portfolio shift. Similarly, when you add money, it needs to be allocated. You don't need to worry about that, as our rebalancing algorithm does it for you. Our algorithm is well-tested and in line with advanced finance literature. It is designed to add some small net gains +/- 0,15 % depending on the portfolio.

An Overview of Our Three Different Portfolios

As you can see, we have done a lot of research on how to pick the right ETFs. To save you this work and to make it as easy as possible for you to invest and build wealth for a secure retirement, we have created three fundamental portfolios for you.

All three portfolios outperform the MSCI World benchmark. Which one is best for you depends on your personal preferences. You can also mix these portfolios to create your portfolio. In your personal client dashboard, you can adjust the preferences that lead to different mixes of our portfolios.

Here are our portfolios at a glance:

1. Global Portfolio: Our Global Portfolio includes large- and small-cap companies and provides broad exposure to global markets. This portfolio provides competitive returns while maintaining low expenses.

2. Global Green Portfolio: The Global Green Portfolio is designed for investors who prioritize sustainable and environmentally responsible investments. It consists of companies that contribute to the global green economy and have strong growth potential.

3. Euro Green Portfolio: Designed for investors seeking a European focus, the Euro Green Portfolio includes a mix of global large-cap companies and European-based companies. This portfolio is denominated in euros and adheres to environmental, social, and governance compliance standards (ESG).

Over the long run, a stock market index that accurately reflects the economy tends to grow in line with the nominal output (GDP). Additionally, it considers dividend yield and cash buybacks. At Pensionfriend, we strive to identify an index that captures real-world growth, combining expected economic growth of 3-4 %, inflation of 2 % in the base economy, and a dividend cash-buyback yield of 2-3 %. In total, this amounts to an anticipated return of 8 %.

To this, one must add any long-term exchange rate movement for a non-Euro-denominated portfolio, the expected Tracking Difference of the ETF (cost minus index outperformance), and any rebalancing benefit.

In the short term, there can be very significant volatility in the value of indices. In theory, it should be merely changes in the above variables and the key alternative investment (fixed interest rate products like government bonds) that drive the valuations. Of these, we focus mainly on the interest rate, as other factors are difficult to predict. It is extremely difficult to be successful at market timing.

Contrary to popular belief, our data analysis challenges the notion that the MSCI World Index or the broader MSCI All Countries Index is the best representation of global growth. Our own Global and Global Green portfolios have a historical track record of outperforming the MSCI World Index by more than 2 %. This outperformance can be attributed to several factors, including the tracking difference before ETF expenses (more than 0,25 %), rebalancing benefits (more than 0,1 %), careful index selection (more than 1,75 %), and slightly higher ETF expenses (approximately +/- 0,15 %). These higher costs are due to the management of small-cap ETFs, which have relatively higher fixed costs. However, our large-cap ETF costs only 0,07 %, significantly less than the MSCI World ETF.

While our Global and Global Green portfolios can potentially exceed the calculated 8 % return, we are cautious about setting expectations. Historical performance shows rates exceeding 10 % (over 8 % in inflation-adjusted terms). However, we do not recommend assuming such high returns. Over time, equity markets have become more liquid and efficiently priced, limiting the likelihood of significant further growth in liquidity premia.

At Pensionfriend, we use our expertise to unlock the long-term growth potential of stock market indices by constructing portfolios that balance growth opportunities with prudent risk management.

Your next steps:

Also, check our adjoining articles to see that we keep the cost as low as possible and that the taxes are such that the Private Pension Plan makes for the best solution to supplement your public pension.

Also, check our calculators and dashboard to see how much you need and want to contribute.

Seek an appointment with an advisor to put all the dots on the i's, have your special questions answered, and get on the way to a safe and sound financial future. Waiting is costly!